PASADENA, Calif. – Not that long ago, real estate agents and their home sellers could command top dollar and then some thanks to a pandemic-fueled buying frenzy.

It wasn’t unusual to hear sellers requesting that buyers waive the appraisal contingency (boilerplate language in the residential purchase agreement). Or waive potentially expensive repair contingencies that a home inspector might discover after the buyer has signed on the dotted line. Or waive the loan approval contingency. Waive. Waive. Waive.

Whatever the buyer waives upfront could mean he or she is at risk of forfeiting the earnest money deposit (of the sales price) if the buyer cannot or will not complete the sale.

Today, the shoe is on the other foot. Homebuyers have their own high-minded demands such as requesting sellers pay for repairs or pay for termite trouble. And oh yes, pay all the closing costs. Pay. Pay. Pay.

They can even ask a seller to help them pay down the rising interest rates.

Why and how, you ask?

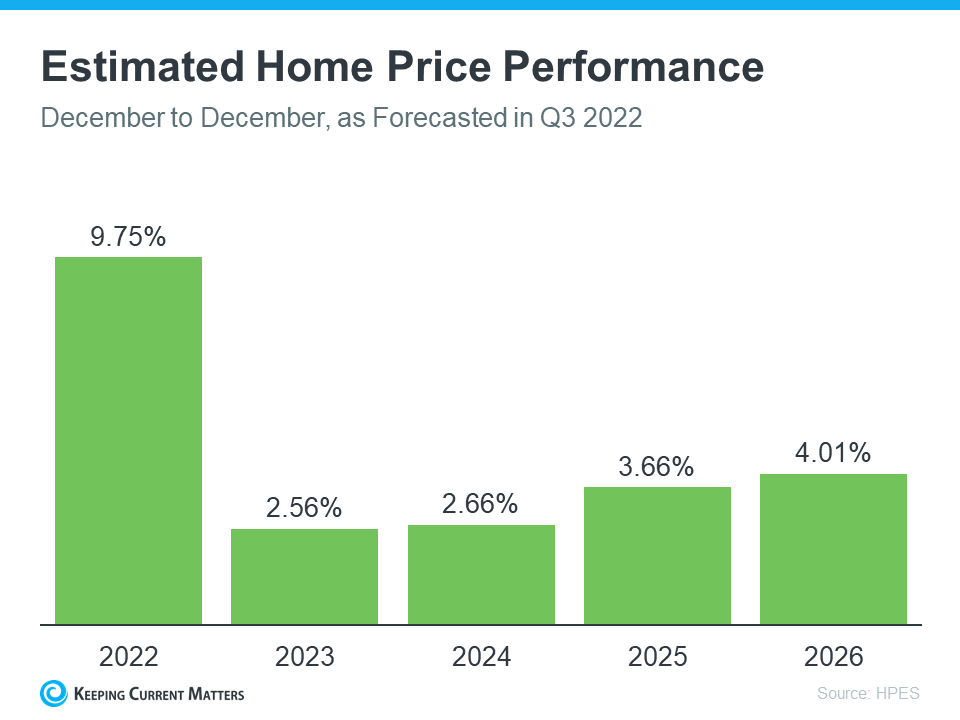

Fixed-rate mortgages have more than doubled in the last nine months, making fixed-rate payments painfully higher and less affordable. This week, the average Freddie Mac 30-year fixed rate stands at 6.66% compared with 3.22% back on Jan. 6. Consequentially, home sales have s-l-o-w-e-d down and median home prices are flattening.

Mortgage lenders are bringing back a sometimes-popular loan program used in times of climbing interest rates. Called a 2-1 buydown or temporary buydown, it’s a way to lower interest rates and subsequently the buyers’ mortgage payment for the first two years – ideally at the seller’s expense.

Here’s how it works: Say you can get a 30-year fixed rate without points at 6.625%. A 2-1 buydown would have your principal and interest payment at 4.625% for the first 12 months and 5.625% for the second 12 months. After the first two years, the interest rate rises to 6.625% for the remaining life of the 30-year mortgage.

On a $600,000 loan balance, the year-one principal and interest payment at 4.625% would be $3,085. The year-two principal and interest payment at 5.625% would be $3,454. The year-three principal and interest payment and the remainder of the loan would be $3,842.

The cost for year one is 12 x $757 or $9,084 (difference between 4.625% monthly payment of $3,085 and 6.625% or $3,842). The cost for year two is 12 x $388 or $4,656 (difference between 5.625% monthly payment of $3,454 and the 6.625% or $3,842). The total buydown cost is $13,740 or 2.3% (points) of the loan amount.

How does this get paid? The effective interest rate during the early years of the mortgage is reduced because of the deposit of a lump sum of money, sometimes called a subsidy. Fannie Mae guidance states these Interested Party Contributions or IPCs may be paid for by the property seller, the borrower’s employer, the mortgage lender, the borrower or other interested parties (real estate agents, for example).

This subsidy goes into an escrow impound account controlled by the loan servicer. The account balance is reduced each month as the subsidy is added as part of the temporarily reduced monthly mortgage payment.

The borrower does have to qualify at the 6.625% note rate.

Let’s say you have an agreeable seller offering to pay all the buyer’s ordinary closing costs of $6,000, for example. Termite and other repairs come to $5,000. And don’t forget about the buydown costs of $13,740. This comes to a total of $24,740.

For a principal residence or a second home, the maximum IPC is 9% of the sales price (not the loan amount) when the buyer is making a down payment of at least 25%. It falls to 6% IPC when the down payment is less than 25% or as little as 10%. The IPC drops to 3% when the buyer is putting less than 10% down. Also, the IPC is restricted to 2% on any investment property purchases.

In the $600,000 loan amount example above, the allowable IPC would mathematically work if the borrower were putting at least 10% down on an owner-occupied purchase. If it’s less than 10% down or an investment purchase, the totals are over Fannie Mae limits. The seller can contribute up to the limit but not more.

In my opinion, a recession is highly likely next year. What happens if mortgage rates drop within the next two years, and you want to refinance to a lower rate?

Any remaining subsidy balance is owned and credited to the borrower, reducing the payoff balance by the remaining amount of the subsidy. For example, the remaining loan balance is $575,000. The subsidy remaining in the escrow impound account is $5,000. The payoff demand statement would show a loan balance of $570,000.

But what if home prices also fall? Can you still refinance? Perhaps.

When refinancing, the loan-to-value ratio will be based on the loan balance divided by the current property value. Fannie does allow refinances up to 95% loan-to-value. Less equity potentially means more lender pricing hits called loan-level pricing adjustments. And there’s a chance of having to pay mortgage insurance or a higher amount of mortgage insurance if your loan balance drops below 80% loan-to-value.

“While we are seeing deceleration in appreciation, we are not seeing large drops in value (coming),” said Don Chiesa, a senior vice president at Rocket Mortgage. (Full disclosure: My firm Mortgage Grader is a Rocket customer.)

Copyright © 2022 Pasadena Star-News. Jeff Lazerson is a mortgage broker.

©Florida Realtors®

Recent Comments